Last week we defined TennCare and how it applies to our clients. This week I want to go more in-depth with how TennCare serves Tennesseans with long-term care.

Many people believe that Medicare benefits will cover nursing home care once an individual is 65 or older, but this simply isn’t true. While Medicare covers the first 100 days, it doesn’t cover long-term assisted living. Read more about Medicare here.

“ Choices” is Tennessee’s Medicaid program for long-term care services and support

Back to TennCare/Medicaid…

My Mom doesn’t have long-term healthcare insurance. What are my options?

Payout of pocket until you run out of cash – This is an unrealistic option for most families. Nursing home care is expensive. Not a lot of people have an extra $7,000-$11,000 a month in their bank accounts.

Do a reverse mortgage on her home.

Qualify for the TennCare / Medicaid program called “CHOICES”.

As you can see, options 1 and 2 are very unpleasant and leave nothing left for a loved one’s legacy. However, option 3, CHOICES, is definitely something worth looking into.

What is CHOICES?

CHOICES is the category of TennCare that provides Long-Term Services and Supports (LTSS) such as nursing home care.

What is the process for getting qualified for CHOICES?

In order to be eligible to receive benefits from TennCare/Medicaid your loved one must first qualify within these three categories:

Medical eligibility

Income threshold

Asset threshold

Being medically and financially eligible is necessary for TennCare approval

How does someone become medically eligible for TennCare CHOICES?

The state of Tennessee will determine who is medically eligible to receive TennCare Long-Term Services and Support (LTSS) by using a pre-admission evaluation (PAE). This PAE is used to determine if the applicant can do basic life skills on their own without help. The PAE will also determine if the applicant is safe in their current environment.

The PAE is a strict evaluation and it is performed on a case-by-case basis. An applicant must receive a score of 9 or higher on a 26 point scale in order to be considered medically eligible for TennCare Long-Term Support Services.

For example, a caregiver or healthcare provider may be asked about a patient’s level of ability to do things and how much assistance is needed.

The following Activities of Daily Living (ADLs) are covered in the PAE evaluation:

Transfering

Mobility

Communication

Medication

Orientation

Eating

Behavior

If you or your loved one is unlikely to get to a nine or higher on the PAE, it is always appropriate to ask for a “safety determination” evaluation as an alternative route of becoming medically eligible for Choices.

How can someone become financially eligible to receive CHOICES?

You must be able to prove that the applicant has a low income and little assets. As of January 2022, an individual applying for TennCare CHOICES cannot have an income exceeding $2,523.00 per month. Additionally, the applicant cannot have more than $2,000 in assets. This includes any money in the bank and investment accounts but also requires consideration of retirement accounts, life insurance policies, real estate, artwork, jewelry, and any other valuables. When we talk about the assets for a couple of things get a little more complex. The most important thing is that both the applicant and their family are taken care of, both medically and financially.

My Mom is over the limits for income and assets? What do we do?

If the applicant is in excess of the amounts we can plan for that! We have a tool to help people who have excess income and assets yet need to qualify for TennCare/Medicaid called the “Care and Savings Assessment”. With this Care and Savings Assessment, we work to determine the best way to structure you or your loved one’s finances, either now or in the future. We plan so that our clients have the peace of mind knowing they can qualify for TennCare if and when they need it!

In conclusion

It is often helpful to have an attorney assess your financial situation and offer recommendations on how those finances may be restructured to qualify for TennCare Long-Term Services and Support (LTSS). As an experienced TennCare planning attorney, I can help you evaluate your risk and create a plan that takes care of everyone in the family.

Are you ready for help with TennCare planning? Contact us and we can discuss your plan. Next week we will go over some examples of how we restructure an individual’s finances to meet their needs for long-term care.

When one spouse wants to disinherit the other, but they are still married, it can be a complicated process. In most cases, disinheriting a spouse is only possible if you have a valid prenuptial agreement or if you are divorced.

Let’s illustrate this with an example:

Jack and Jill have been married for five years, and have one child together. Their house was purchased by Jill before they were married, and Jack’s name was never added to the deed.

Jill recently discovered that Jack is cheating on her with the Instacart shopper. She and Jack are now separated and have started the divorce process, but she wants to make sure that if she dies before the divorce is final that Jack won’t get anything from her.

What can Jill do?

Jill can disinherit her spouse after the divorce

Unfortunately, Jill cannot disinherit Jack until she files for divorce. Tennessee law does not allow you to disinherit your spouse- even if you write a will that says that! My advice is to get divorced as quickly as possible. Unless divorced, Jack is entitled to his share.

The good news is that once divorce papers have been filed, there will be an automatic injunction that specifies that the pair no longer have spousal rights on the property through marriage. This is primarily to protect things like bank accounts, real estate, relationships with the children, and health insurance coverage. However, all that does is prevent money from being spent by either spouse outside of regular expenses. Jill won’t be able to do anything, like estate planning, until after the divorce has been settled or through special permission from a judge.

In the meantime, there are still a few steps Jill can take:

Utilize her prenuptial agreement

Jack and Jill signed a prenuptial agreement prior to their marriage. In it, they waived the right to inherit from each other. All Jill needs to do now is to rewrite her will to specifically omit Jack.

Divide assets into separate trusts

Jill can establish a trust under her name and place the house in it. Since Jack’s name isn’t on the deed or on the trust, he has no right to the house if Jill were to pass before the divorce is finalized.

Rewrite her will

Jill can rewrite her will so that Jack only gets what he is entitled to by law, called his elective share. In Tennessee, spouses are entitled to a homestead allowance, a year of support, and elective share. The elective share amount depends on how long you are married.

Hire a family law attorney

The divorce will go much quicker with the help of a family law attorney.

Jill can get a jump start on planning her estate.

Finally, if Jill is preparing for a divorce, she can take advantage of all the legal documents at her fingertips and get a head start on creating the estate plan she desires. Once her divorce decree is finalized, she can meet with her lawyer and sign the document to make it valid.

Are you getting a divorce and want to start over with your own will and estate plan in Tennessee? Are you looking for a referral to a family law attorney? Let us know! We are happy to help you make plans for your new life. Not sure where to start? Give us a call. We offer a complimentary 15-minute call to see if we are the right fit for you and your situation. You can schedule your call by clicking here.

A Davidson County will and trust lawyer’s job is to make sure that you have all of your ducks in a row so that if you become incapacitated or die, your loved ones will know how to manage your estate and follow your wishes. Laws in Tennessee vary from those found around the country, which is why you want to work with an attorney who is skilled in understanding your specific needs. One area that should be considered is your service providers.

Make a list of your service providers and put it in your estate plan

“Service providers” covers a wide range of individuals involved in your life. Should you be unable to communicate with them, you want to ensure that your trustee, executor, conservator, or other responsible person is able to communicate with them on your behalf. Having them all listed in one place will make this job much more manageable.

Household Providers

This list should include all of the people or companies that you deal with when it comes to the maintenance of your home. In some cases, your home will need to continue to function in your absence, and your representative will need to be able to contact these people to make sure things keep running smoothly. In other cases, whether you are deceased or incapacitated, there are certain services that you may no longer need, and the person in charge needs to be able to contact the service providers and cancel with them.

Some examples of household providers that you will want to list might include:

Computer support

Food or water delivery

Gardening

Pet care

Housekeepers

Heating/Cooling system maintenance

Heating oil delivery

House sitters

Pest control

Pool or spa maintenance

Utilities

Vehicle maintenance

Basically, anything that you have performed on a regular basis should be noted, along with contact and payment information.

Medical Service Providers

You should also provide your representative with contacts for your medical service providers. This information could be very valuable should you need medical attention but be unable to reach out to these providers on your own. Additionally, if you have standing appointments with these providers, it will be helpful to have them canceled so you don’t accrue charges for services you’re not using.

Some of the medical service providers you may want to include on your list are:

Chiropractor

Counselor

Dentist

Massage therapist

Ophthalmologist

Physical therapist

Primary care physician

Psychiatrist

Specialists

Personal Service Providers

There are other types of regular services that you may use, and you’ll want to include these as well for the same reasons already mentioned. Some personal service providers to keep in mind for inclusion:

Childcare provider

Hairdresser

Home care provider

Meal preparation

Transportation

Tutors

Additional Information

Along with the contact information for these service providers, it’s a good idea to make notes about when they are expected, and you may even want to include service agreements and contracts. For example, if you have a standing arrangement to have your sprinkler system blown out each fall, make a note of that.

Your estate planning attorney may not include all of this information directly in your estate plan, but they will want to be able to assist your family with where it can be located when the need arises.

If you are seeking estate planning services, please book a call with our office here .

This month we will discuss the subject of powers of attorney. In week one, we will discuss how to name a financial power of attorney. This is also known as a durable power of attorney.

There are many things to consider when appointing a financial power of attorney (aka an attorney-in-fact). This is an important position. Whoever you appoint would have the ability to make decisions regarding how you manage your finances. While it may seem obvious, it’s important to focus on choosing someone who is organized, trustworthy, and financially responsible.

What powers does an agent have when they have a financial power of attorney?

As stated earlier, the agent with a financial power of attorney can handle your finances just as you can. An agent will have the ability to go to your bank and handle banking transactions. They can contact your investment account broker and manage those funds. They can handle your insurance and sell your house. Of course, you want your agent to only make financial transactions in your best interest while you are incapacitated.

Can things go horribly wrong? Yes! Your agent has the power to clean out all of your bank accounts and sell your home. Heck, if they wanted to, they could take your assets, move to Fiji, and set up a little beach bar! I want to reiterate: It’s important that you choose someone who would never even think of doing something like that. You need to choose someone who will only have your best interest at heart.

Who should be your financial power of attorney?

When considering who should serve as a financial power of attorney, a lot of people are compelled to choose someone close to them. A lot of times this will be a relative, such as your children or possibly a sibling, but it doesn’t have to be. The agent could also be a close friend or even a professional if that is who fits that role in your life. In our practice, we like to make sure that our client acknowledges this very important point: the person you name as your agent in a financial power of attorney will have the ability to handle your finances pretty much the same as you will.

Choose an agent who can communicate effectively

Not only do you need to trust your agent, but we also recommend that you find someone that other people trust! While this element is not completely necessary, it may be important to you that your agent be relied upon to communicate important information effectively with the people in your life.

For example, if one of your relatives says to your agent: “Hey, my Aunty saved a lot of money and invested it well, how much does she have now and what has the spent money been used for?”. Ideally, you would have an agent that relatives intuitively trust to spend your funds in your interest. However, it would be really awesome if your agent took the time out of their day to respond thoroughly to your relative’s questions.

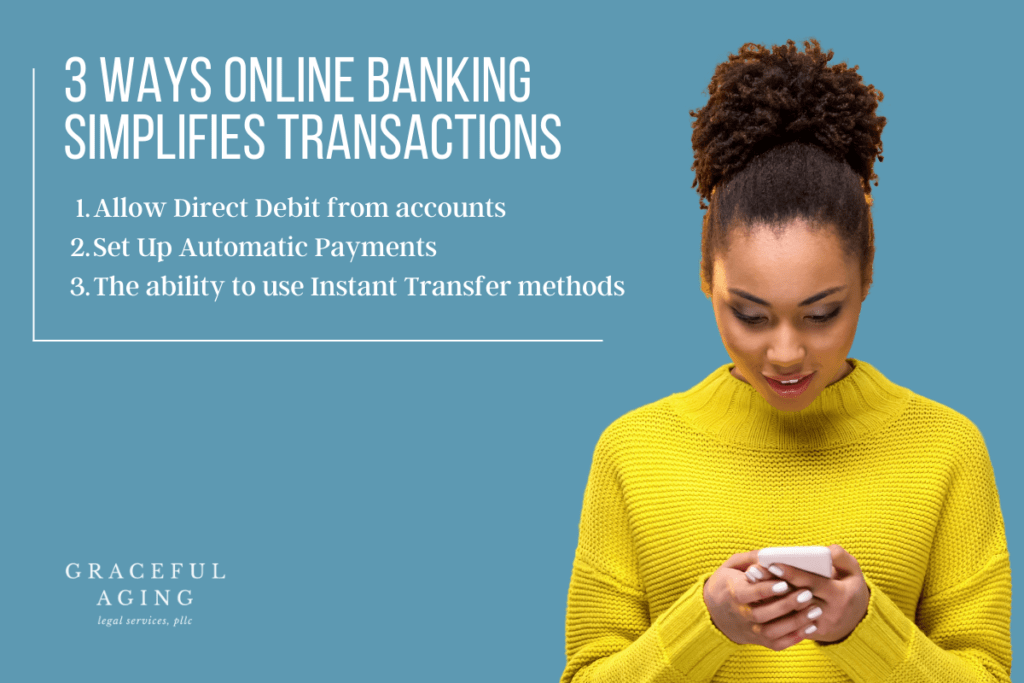

Choose an agent that is comfortable with online banking

Your agent should be good at bookkeeping

In a perfect world, your agent with financial powers of attorney would be held accountable for the transactions coming out of your assets. A good agent can effectively answer questions about spending and back it up with good bookkeeping!

An agent with power of attorney does not have to live in your state

As we mentioned before, the era of digital banking is here and it allows us the option to choose from a larger pool of agents, regardless of their location. Now, many people think that their agent under a power of attorney cannot be someone who lives out of state. And that is simply not true. Sometimes it helps to have somebody who lives in the state, but that is not a requirement in Tennessee. We do so many things by email and telephone, texting, and online business transactions that your financial power of attorney person, your agent, will likely be handling any business transactions online.

Choose an agent who will outlive you

While this is not a requirement, it is a good idea to think about someone who will outlive you. Generally, when you are using your power of attorney, it’s when you’re incapacitated. While there are times when a durable power of attorney is used on a temporary basis, such as during a medical event, it is more likely going to be during a period when we are at the end of our lives and are experiencing some type of ongoing health condition that is not likely to improve. We recommend that you look for an agent who can help on a continuing basis. A well-suited agent allows everyone to relax and enjoy the time you have left on this earth.

Who should NOT be your durable power of attorney

Again, while it may seem obvious, it is important to reiterate that anyone who is untrustworthy, unlikeable, terrible with money, incapable of balancing a checkbook, or unable to effectively use online banking might not be the best choice for becoming an agent of financial power of attorney. The goal is to find someone who can keep good accounting records and knows exactly where your money went, down to every last penny! A good agent is someone who is willing to communicate with everyone without hesitation. The main point is that no one in your circle should be concerned that your agent is taking advantage of you if you are incapacitated.

Now, if you are not incapacitated, your agent should only be acting if you are telling them to do so. Even if you have your power of attorney take effect immediately, your agent can and should only act under your direction. If you find that the agent acts otherwise, there are legal actions you can take against them in court.

In conclusion

A power of attorney is a useful tool for organizing the “adulting” part of your life, especially in incapacitation. A financial power of attorney should be someone that you absolutely trust; someone who will not give pause to others in your life. Someone who is financially responsible and organized, and someone who is familiar with handling online transactions. It does not matter if your agent lives in your state. In short, find an agent you believe will always have your best interest at heart.

There are many types of powers of attorney. Many powers of attorney are used when creating a well-thought-out estate plan. Do you think you could use a durable power of attorney in Nashville? Schedule an initial call to see if we can help you with your situation.

Disclaimer

This website is an attorney advertisement. It is not legal advice and does not create an attorney-client relationship with the viewer.